English

English  Español

Español  Portugues

Portugues  Français

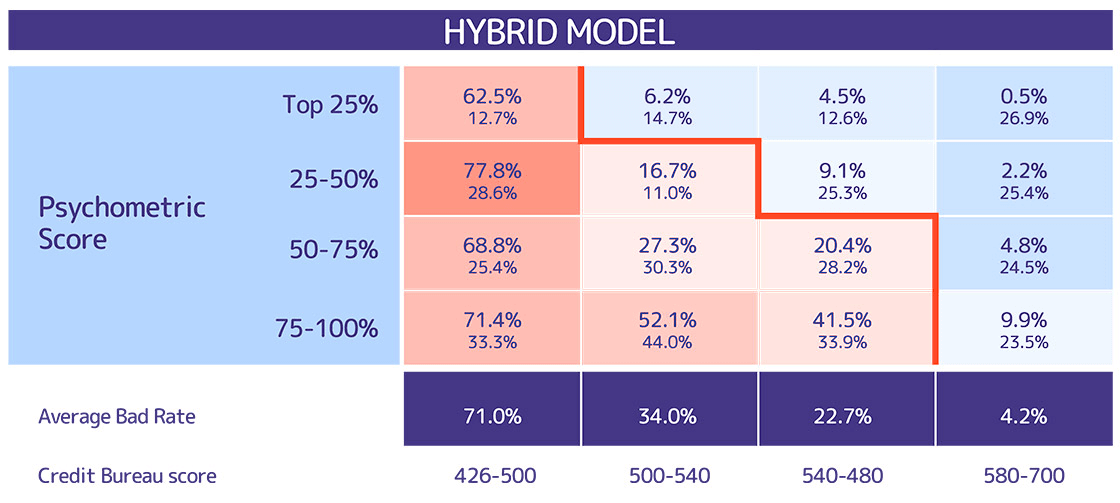

Français COREMETRIX worked together with a credit card issuer to improve access to conventional credit among the neglected consumers that did not met the standards of the current credit policy. We support the Client’s primary goal of increasing market share by increasing the applicants’ acceptance rate without affecting the company’s level of risk. Our team created a hybrid model that combines the traditional score provided by a Credit Bureau and the psychometric score. The COREMETRIX solution identified a significant proportion of rejected customers who were within the appetite of Customer’s risk. By applying psychometric data, the Client experienced an increase in access to their services without incorporating any additional risk, and even reducing it in some new segments to be incorporated.